All Categories

Featured

Table of Contents

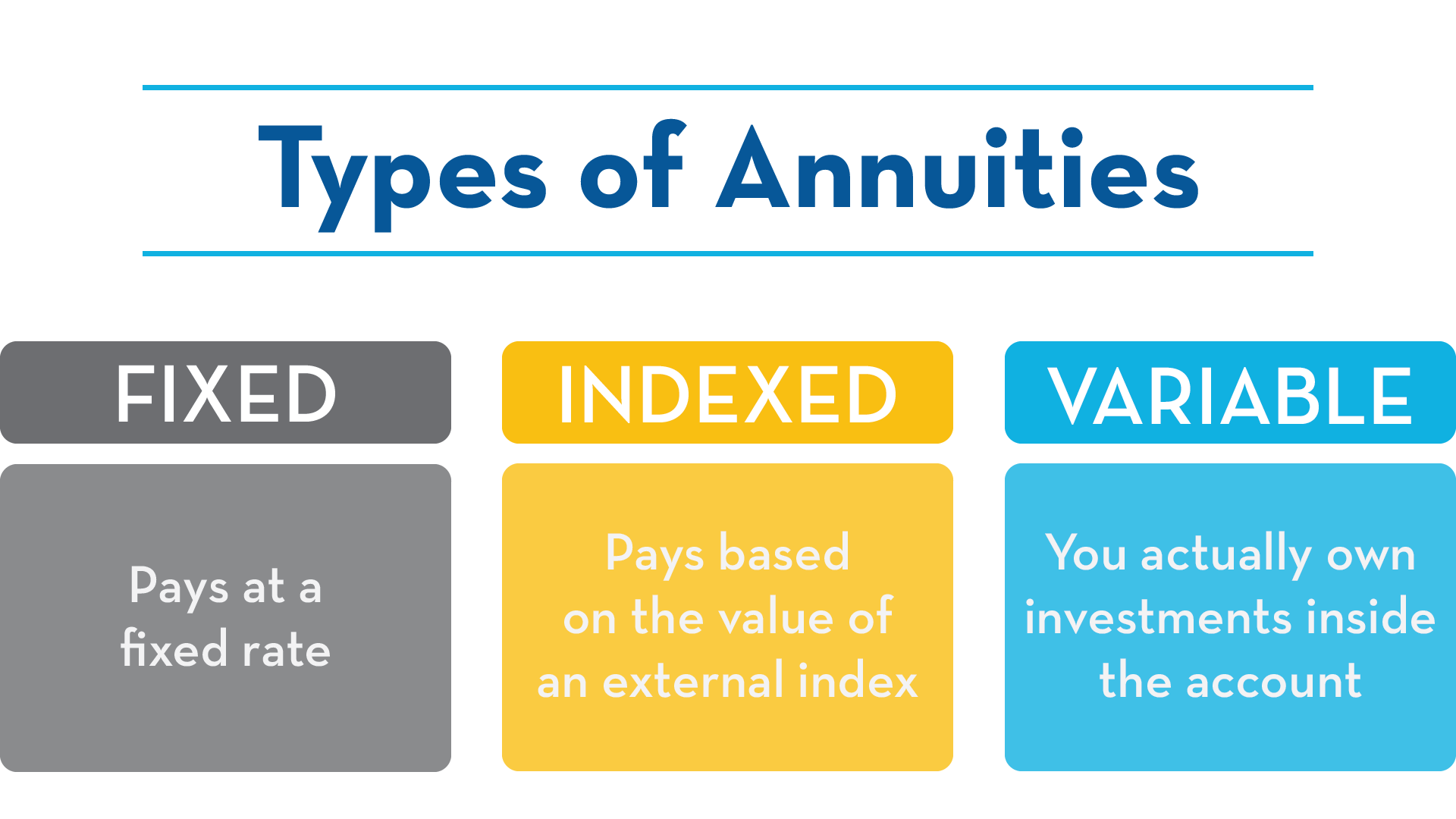

Fixed or variable development: The funds you contribute to deferred annuities can grow over time., the insurance coverage firm sets a particular portion that the account will earn every year.

A variable annuity1, on the various other hand, is most frequently connected to the investment markets. The growth could be greater than you would certainly access a set price. But it is not assured, and in down markets the account can decline. No. An annuity is an insurance coverage product that can aid assure you'll never lack retired life savings.

It's regular to be worried concerning whether you've saved sufficient for retired life. Both Individual retirement accounts and annuities can assist relieve that problem. And both can be used to build a robust retirement method. Understanding the distinctions is crucial to maximizing your savings and preparing for the retirement you are worthy of.

Over years, small contributions can expand extensively. Beginning when you are young, in your 20s or 30s, is crucial to obtaining one of the most out of an individual retirement account or a 401(k). Annuities convert existing financial savings into ensured settlements. If you're not exactly sure that your cost savings will certainly last as long as you require them to, an annuity is a great way to minimize that issue.

On the various other hand, if you're a long way from retirement, beginning an individual retirement account will be valuable. And if you've contributed the optimum to your individual retirement account and would love to place extra cash toward your retirement, a deferred annuity makes good sense. If you're uncertain about just how to handle your future savings, a financial professional can aid you get a more clear image of where you stand.

Decoding How Investment Plans Work A Comprehensive Guide to Fixed Vs Variable Annuity Pros Cons Defining Annuities Fixed Vs Variable Advantages and Disadvantages of Deferred Annuity Vs Variable Annuity Why Fixed Annuity Vs Equity-linked Variable Annuity Can Impact Your Future How to Compare Different Investment Plans: How It Works Key Differences Between Fixed Annuity Or Variable Annuity Understanding the Risks of Indexed Annuity Vs Fixed Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Fixed Income Annuity Vs Variable Annuity A Closer Look at Variable Annuity Vs Fixed Indexed Annuity

When thinking about retired life preparation, it is very important to discover a strategy that ideal fits your lifefor today and in tomorrow. might help ensure you have the earnings you need to live the life you want after you retire. While repaired and taken care of index annuities sound comparable, there are some vital distinctions to arrange through before picking the best one for you.

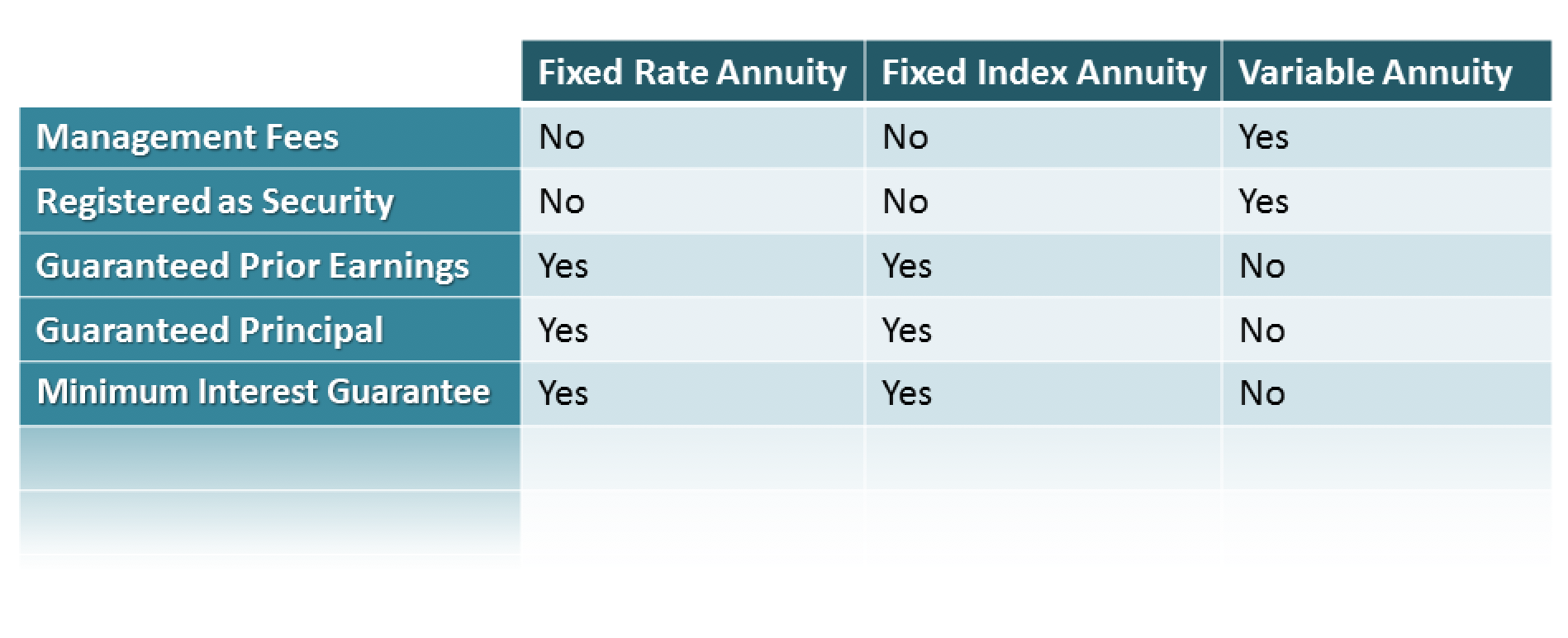

is an annuity contract developed for retirement income that guarantees a fixed rates of interest for a specified time period, such as 3%, despite market efficiency. With a set rate of interest, you understand beforehand exactly how much your annuity will expand and just how much income it will pay.

The profits may be available in fixed settlements over a set variety of years, repaired repayments for the remainder of your life or in a lump-sum repayment. Revenues will not be taxed until. (FIA) is a kind of annuity agreement developed to create a steady retired life income and enable your possessions to expand tax-deferred.

This produces the potential for more growth if the index executes welland alternatively uses protection from loss because of bad index efficiency. Although your annuity's passion is linked to the index's performance, your money is not directly purchased the marketplace. This suggests that if the index your annuity is tied to does not perform well, your annuity does not lose its worth because of market volatility.

Set annuities have actually an assured minimum interest rate so you will certainly obtain some interest each year. Fixed annuities might tend to pose less financial risk than various other types of annuities and financial investment products whose worths increase and drop with the market.

And with particular kinds of fixed annuities, like a that fixed interest rate can be locked in via the whole agreement term. The interest made in a dealt with annuity isn't affected by market variations for the period of the set period. As with the majority of annuities, if you want to withdraw money from your dealt with annuity earlier than set up, you'll likely incur a charge, or give up chargewhich in some cases can be large.

Exploring Indexed Annuity Vs Fixed Annuity Everything You Need to Know About Financial Strategies Breaking Down the Basics of Investment Plans Benefits of Variable Vs Fixed Annuity Why Choosing the Right Financial Strategy Is a Smart Choice Variable Annuity Vs Fixed Indexed Annuity: How It Works Key Differences Between Different Financial Strategies Understanding the Risks of Fixed Vs Variable Annuity Pros And Cons Who Should Consider Strategic Financial Planning? Tips for Choosing Immediate Fixed Annuity Vs Variable Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Fixed Vs Variable Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at Variable Annuity Vs Fixed Annuity

On top of that, withdrawals made prior to age 59 may be subject to a 10 percent government tax obligation charge based upon the fact the annuity is tax-deferred. The rate of interest, if any kind of, on a set index annuity is linked to an index. Because the interest is tied to a stock exchange index, the rate of interest attributed will either advantage or experience, based upon market performance.

You are trading potentially taking advantage of market growths and/or not maintaining speed with inflation. Fixed index annuities have the benefit of potentially providing a higher guaranteed rate of interest when an index does well, and principal security when the index endures losses. For this defense versus losses, there might be a cap on the optimum earnings you can obtain, or your earnings may be limited to a percentage (for instance, 70%) of the index's adjusted value.

It commonly likewise has a current rate of interest as stated by the insurance provider. Passion, if any kind of, is linked to a defined index, as much as a yearly cap. An item might have an index account where interest is based on exactly how the S&P 500 Index does, subject to a yearly cap.

Passion earned is dependent upon index performance which can be both positively and negatively affected. In addition to recognizing taken care of annuity vs. fixed index annuity distinctions, there are a few various other kinds of annuities you might want to explore before making a choice.

{kind=link}

Table of Contents

Latest Posts

Analyzing Strategic Retirement Planning A Comprehensive Guide to Investment Choices What Is the Best Retirement Option? Benefits of Choosing Between Fixed Annuity And Variable Annuity Why Fixed Vs Var

Analyzing Strategic Retirement Planning Everything You Need to Know About Fixed Annuity Vs Variable Annuity Defining Fixed Index Annuity Vs Variable Annuity Pros and Cons of Fixed Index Annuity Vs Var

Exploring Fixed Annuity Vs Variable Annuity A Comprehensive Guide to Fixed Annuity Or Variable Annuity Defining the Right Financial Strategy Benefits of Pros And Cons Of Fixed Annuity And Variable Ann

More

Latest Posts